Chapter 6 Cost of Capital

Chapter 6 Cost of Capital

Download as pptx, pdf, or txt

You might also like

- CH 11Document93 pagesCH 11dsfsdfNo ratings yet

- Topic 2 ExercisesDocument6 pagesTopic 2 ExercisesRaniel Pamatmat0% (1)

- Chapter Three: Valuation of Financial Instruments & Cost of CapitalDocument68 pagesChapter Three: Valuation of Financial Instruments & Cost of CapitalAbrahamNo ratings yet

- Advanced Accounting Part 2 Business Combinations (Ifrs 3)Document10 pagesAdvanced Accounting Part 2 Business Combinations (Ifrs 3)ClarkNo ratings yet

- Cost of Capital Lecture Slides in PDF FormatDocument18 pagesCost of Capital Lecture Slides in PDF FormatLucy UnNo ratings yet

- Old Exam Questions - Cost of Capital - Solutions Page 1 of 42 PagesDocument42 pagesOld Exam Questions - Cost of Capital - Solutions Page 1 of 42 PagespepeNo ratings yet

- Performance 6.10Document2 pagesPerformance 6.10George BulikiNo ratings yet

- A. The Importance of Capital BudgetingDocument98 pagesA. The Importance of Capital BudgetingShoniqua JohnsonNo ratings yet

- Managing Current Asset Ch.8Document34 pagesManaging Current Asset Ch.8AimanNo ratings yet

- Overview of Financial ManagementDocument16 pagesOverview of Financial ManagementKAUSHIKNo ratings yet

- 6 Dividend DecisionDocument31 pages6 Dividend Decisionambikaantil4408No ratings yet

- Cost of CapitalDocument18 pagesCost of CapitalJoshua Cabinas100% (1)

- Cost II Chapter ThreeDocument106 pagesCost II Chapter Threefekadegebretsadik478729100% (1)

- Cost of CapitalDocument27 pagesCost of CapitalShashank PandeyNo ratings yet

- Chapter 6 Capital Structure PDFDocument20 pagesChapter 6 Capital Structure PDFmuluken walelgnNo ratings yet

- Capital Investment AppraisalDocument30 pagesCapital Investment Appraisalzahiraqasrina100% (1)

- FM II, CH 4, Managing Current AssetsDocument82 pagesFM II, CH 4, Managing Current AssetsObsa KamilNo ratings yet

- International Capital Budgeting and Cost of CapitalDocument50 pagesInternational Capital Budgeting and Cost of CapitalGaurav Kumar100% (2)

- Cost of CapitalDocument17 pagesCost of CapitalKunal GargNo ratings yet

- Chapter 5 GF&SRFDocument17 pagesChapter 5 GF&SRFGosaye Abebe100% (1)

- Chapter 3 Valuation and Cost of CapitalDocument92 pagesChapter 3 Valuation and Cost of Capitalyemisrach fikiruNo ratings yet

- Investment Appraisal Techniques 2Document24 pagesInvestment Appraisal Techniques 2Jul 480wesh100% (2)

- Corporate Valuation and Value Based ManagementDocument10 pagesCorporate Valuation and Value Based ManagementjhatpatzeroNo ratings yet

- Time Value of MoneyDocument52 pagesTime Value of MoneyJasmine Lailani ChulipaNo ratings yet

- Chapter 20 - AnswerDocument15 pagesChapter 20 - AnswerAgentSkySky100% (1)

- Project Analysis and Evaluation: Dr. Agim MamutiDocument27 pagesProject Analysis and Evaluation: Dr. Agim MamutiZubair AsamNo ratings yet

- Accounting For LeasingDocument36 pagesAccounting For LeasingAKSHAJ GOENKANo ratings yet

- Molson Coors Case StudyDocument27 pagesMolson Coors Case StudyDuc Manh50% (2)

- FM11 - CH - 06 - Bonds and Their ValuationDocument49 pagesFM11 - CH - 06 - Bonds and Their ValuationAneesaNo ratings yet

- Investment Analysis CODocument4 pagesInvestment Analysis COMIKIYAS BERHENo ratings yet

- Advanced Financial Accounting - II CH 1-4Document24 pagesAdvanced Financial Accounting - II CH 1-4TAKELE NEDESANo ratings yet

- 07 Capital Structure and LeverageDocument25 pages07 Capital Structure and LeverageRishabh SarawagiNo ratings yet

- Corp Finance Group One Course Work (Final)Document27 pagesCorp Finance Group One Course Work (Final)jonas sserumagaNo ratings yet

- FM - Chapter 4, Return and RiskDocument31 pagesFM - Chapter 4, Return and RiskDaniel BalchaNo ratings yet

- MA2 T2 MD Cost of CapitalDocument57 pagesMA2 T2 MD Cost of CapitalMangoStarr Aibelle VegasNo ratings yet

- Principles of AccountingDocument12 pagesPrinciples of AccountinggrfNo ratings yet

- Estimating The Optimal Capital StructureDocument22 pagesEstimating The Optimal Capital StructureAqeel Ahmad KhanNo ratings yet

- Audit UNIT 3Document11 pagesAudit UNIT 3Nigussie BerhanuNo ratings yet

- b1 Solving Set 2 May 2018 - OnlineDocument4 pagesb1 Solving Set 2 May 2018 - OnlineGadafi FuadNo ratings yet

- Chapter 4 DerivativesDocument38 pagesChapter 4 DerivativesTamrat KindeNo ratings yet

- SFM CA Final Mutual FundDocument7 pagesSFM CA Final Mutual FundShrey KunjNo ratings yet

- Leverage: Presented by Sandesh YadavDocument14 pagesLeverage: Presented by Sandesh YadavSandesh011No ratings yet

- Financial Modeling Chapter 2 Calculating Cost of Capital 2015Document64 pagesFinancial Modeling Chapter 2 Calculating Cost of Capital 2015NEERAJ N RCBSNo ratings yet

- Advanced FA I - Chapter 01, Accounting For Investment in JADocument58 pagesAdvanced FA I - Chapter 01, Accounting For Investment in JAKalkidan G/wahidNo ratings yet

- CHAPTER 12 Stock ValuationDocument36 pagesCHAPTER 12 Stock ValuationVivi CheyNo ratings yet

- The Baumol ModelDocument3 pagesThe Baumol ModelNoreen DelizoNo ratings yet

- Exercices + Answers (Capital Structure) PDFDocument4 pagesExercices + Answers (Capital Structure) PDFSonal RathhiNo ratings yet

- Prepared by Coby Harmon University of California, Santa Barbara Westmont CollegeDocument38 pagesPrepared by Coby Harmon University of California, Santa Barbara Westmont Collegee s tNo ratings yet

- PSCS CH 9 Accounting For Fiduciary FundDocument5 pagesPSCS CH 9 Accounting For Fiduciary Fundnatnael0224No ratings yet

- Working Capital and Current Assest ManagementDocument84 pagesWorking Capital and Current Assest Managementbusi.kg.tshNo ratings yet

- Chapter-9, Capital StructureDocument21 pagesChapter-9, Capital StructurePooja SheoranNo ratings yet

- Chapter Two: Principles of Accounting and Financial Reporting For State and Local Governments (SLGS)Document55 pagesChapter Two: Principles of Accounting and Financial Reporting For State and Local Governments (SLGS)Bilisummaa GeetahuunNo ratings yet

- Capital Structure TheoryDocument27 pagesCapital Structure Theoryaritraray100% (2)

- Accounting Ratios - Class NotesDocument8 pagesAccounting Ratios - Class NotesAbdullahSaqibNo ratings yet

- Risk and Rate of Returns in Financial ManagementDocument50 pagesRisk and Rate of Returns in Financial ManagementReaderNo ratings yet

- CHAPTER 2 Joint VentureDocument5 pagesCHAPTER 2 Joint VentureAkkamaNo ratings yet

- Chapter 4 Cost of CapitalDocument19 pagesChapter 4 Cost of CapitalmedrekNo ratings yet

- Cost of Capital: Bmbs1024 Accounting and Finance For ManagersDocument18 pagesCost of Capital: Bmbs1024 Accounting and Finance For ManagersRina ZulkifliNo ratings yet

- COST OF CAPITALDocument9 pagesCOST OF CAPITALlabibmahmud93No ratings yet

- Chapter Nine: Cost of Capital & Capital Structure Learning ObjectivesDocument6 pagesChapter Nine: Cost of Capital & Capital Structure Learning Objectivesabraha gebruNo ratings yet

- Index, Slice and Stride: IndexingDocument5 pagesIndex, Slice and Stride: IndexingmedrekNo ratings yet

- CCNAv2 Chapter 05Document18 pagesCCNAv2 Chapter 05medrekNo ratings yet

- CCNAv2 Chapter 09Document39 pagesCCNAv2 Chapter 09medrek0% (1)

- CCNAv2 Chapter 04Document15 pagesCCNAv2 Chapter 04medrekNo ratings yet

- Variables and Mathematical OperatorsDocument2 pagesVariables and Mathematical OperatorsmedrekNo ratings yet

- CCNAv2 Chapter 03Document28 pagesCCNAv2 Chapter 03medrekNo ratings yet

- Formatting Strings: Input InputDocument3 pagesFormatting Strings: Input InputmedrekNo ratings yet

- ABC AnalysisDocument1 pageABC AnalysismedrekNo ratings yet

- ABC Analysis: Item Order Comm. C.. Unit Price Usage Quantity Total Usage Qty Item Rank Cost Order Cumm. % Percentage (%)Document2 pagesABC Analysis: Item Order Comm. C.. Unit Price Usage Quantity Total Usage Qty Item Rank Cost Order Cumm. % Percentage (%)medrekNo ratings yet

- Lab 1.5.1: Cabling A Network and Basic Router Configuration: Topology DiagramDocument41 pagesLab 1.5.1: Cabling A Network and Basic Router Configuration: Topology DiagrammedrekNo ratings yet

- Chapter Six Strategy Analysis and Choice/Strategy FormulationDocument12 pagesChapter Six Strategy Analysis and Choice/Strategy FormulationmedrekNo ratings yet

- Lab 2.5.1: Basic Switch Configuration: TopologyDocument16 pagesLab 2.5.1: Basic Switch Configuration: TopologymedrekNo ratings yet

- Activity 3.5.1: Basic VLAN Configuration NOTE TO USER: This Activity Is A Variation of Lab 3.5.1. Packet Tracer May NotDocument6 pagesActivity 3.5.1: Basic VLAN Configuration NOTE TO USER: This Activity Is A Variation of Lab 3.5.1. Packet Tracer May NotmedrekNo ratings yet

- NIB Bank Business Policy and StrategyDocument29 pagesNIB Bank Business Policy and StrategymedrekNo ratings yet

- AAU SM Chap IIIDocument35 pagesAAU SM Chap IIImedrekNo ratings yet

- Chapter 7 STRDocument10 pagesChapter 7 STRmedrekNo ratings yet

- Chapter 5 STRDocument11 pagesChapter 5 STRmedrekNo ratings yet

- Chapter Two Strategies in ActionDocument9 pagesChapter Two Strategies in ActionmedrekNo ratings yet

- Topic 7 - Equity Market and Stock Valuation QuestionDocument4 pagesTopic 7 - Equity Market and Stock Valuation QuestionJolyn Lee100% (1)

- Stocks and Their Valuation: Features of Common Stock Determining Common Stock Values Efficient Markets Preferred StockDocument40 pagesStocks and Their Valuation: Features of Common Stock Determining Common Stock Values Efficient Markets Preferred StocksidhanthaNo ratings yet

- Clayton, Dubilier - Rice Raises Bid For UDG Healthcare After Investor PressureDocument2 pagesClayton, Dubilier - Rice Raises Bid For UDG Healthcare After Investor PressureSouleïman CisséNo ratings yet

- Nike Inc Cost of Capital Blaine KitchenwDocument11 pagesNike Inc Cost of Capital Blaine KitchenwAlvaro Gallardo FernandezNo ratings yet

- Unit 4 Leverage BuyoutDocument20 pagesUnit 4 Leverage BuyoutJhumri TalaiyaNo ratings yet

- Tata Motors Ratio CalculationsDocument3 pagesTata Motors Ratio CalculationssukeshNo ratings yet

- Mcom Ind As 33 Theory.Document11 pagesMcom Ind As 33 Theory.Umang PatelNo ratings yet

- Numericals On Cost of Capital and Capital StructureDocument2 pagesNumericals On Cost of Capital and Capital StructurePatrick AnthonyNo ratings yet

- Encl: A/aDocument33 pagesEncl: A/aContra Value BetsNo ratings yet

- Assignment On MoneybhaiDocument7 pagesAssignment On MoneybhaiKritibandhu SwainNo ratings yet

- Rolex Rings Limited: ListingDocument3 pagesRolex Rings Limited: ListingAkhil SakethNo ratings yet

- Chapter 03 - How Securities Are TradedDocument8 pagesChapter 03 - How Securities Are TradedSarahNo ratings yet

- Private Equity Guide 1723046539Document33 pagesPrivate Equity Guide 1723046539NickNo ratings yet

- Assignmnet Chapter 13Document12 pagesAssignmnet Chapter 13Nicolas ErnestoNo ratings yet

- Kranav Kapur Investment Project 019Document18 pagesKranav Kapur Investment Project 019Angna DewanNo ratings yet

- Company AuditDocument12 pagesCompany Auditbill78304No ratings yet

- Chapter 5 Statement of Changes in EquityDocument4 pagesChapter 5 Statement of Changes in Equityellyzamae quiraoNo ratings yet

- Accounting For Investments: TheoriesDocument20 pagesAccounting For Investments: TheoriesJohn AlbateraNo ratings yet

- Cost of CapitalDocument4 pagesCost of Capitalkomal mishraNo ratings yet

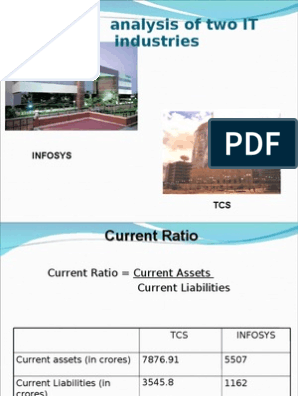

- Comparative Ratio Analysis For TCS and InfosysDocument11 pagesComparative Ratio Analysis For TCS and InfosysChaitanya89% (9)

- BKM CH 03 Answers W CFADocument10 pagesBKM CH 03 Answers W CFAPookguyNo ratings yet

- Lecturenote - 972275618FM II Final EditedDocument101 pagesLecturenote - 972275618FM II Final EditedSujan Bhattarai100% (2)

- Indian Depository RecieptDocument24 pagesIndian Depository Recieptadilfahim_siddiqi100% (1)

- BSE Broker PartnersDocument15 pagesBSE Broker PartnersVernon MonteiroNo ratings yet

- APC Ch9sol.2014Document16 pagesAPC Ch9sol.2014Melissa RiolaNo ratings yet

- Indian Equity MarketDocument26 pagesIndian Equity Marketnavu811No ratings yet

- 8.exercise (Ratio Analysis)Document10 pages8.exercise (Ratio Analysis)Fatema TujNo ratings yet

- 8a.equity Valuation Models - Text Bank (1) - SolutionDocument78 pages8a.equity Valuation Models - Text Bank (1) - Solutionvbnarwade100% (3)

- Chap 012Document23 pagesChap 012princearoraNo ratings yet